CloCo Notes an Innovation in Finance to enable a Climate Alpha and Drive Economic Growth

Energy prices have long dictated the rhythm of the global economy. From oil shocks in the 1970s to the gas crises of the 2020s, volatility in fossil fuel markets has shaped inflation, monetary policy, and the political mood of nations. Even as the world races toward net zero, that dependency has not yet been broken. The question is not whether renewables can provide cheaper power — they already do — but whether the financial and policy frameworks that govern energy markets are keeping up with technological change.

The U.K., like many advanced economies, is discovering that the road to net zero is as much about finance as it is about real world engineering. Behind every turbine and solar farm lies a web of capital costs, long-term contracts, and risk transfers. These are the invisible gears that determine how quickly — and affordably — the energy transition proceeds.

Contracts for difference: the quiet engine of clean power

One of the most successful innovations in the U.K.’s energy transition is the Contract for Difference (CFD), a long-term, two-way financial hedge between companies generating renewable energy and the government. It guarantees generators a fixed “strike price” for their electricity while shielding consumers from price swings. When market prices fall below the strike, the government’s Low Carbon Contracts Company tops up the difference. When prices rise, the generators pay the surplus back to the government.

The result is a rare win-win: predictable revenues for investors, and protection for consumers. According to the UK’s Department for Energy Security and Net Zero (DESNZ), CFDs have saved British households billions in avoided price spikes while dramatically lowering the cost of capital for renewable projects. They have also driven a competitive auction process that slashed strike prices for offshore wind and solar by more than 70 percent in less than a decade.

But the mechanism is not perfect. CFDs were designed for a world in which demand growth was modest and technology costs fell slowly. Neither is true today. Artificial intelligence, electric vehicles, and industrial electrification are driving unprecedented new demand for power — each hyperscale data centre alone can consume as much electricity as a small town of 50,000 people. Simultaneously, the cost of renewables is plunging faster than even government projections anticipated.

The cost revolution in clean energy

Research from the Institute for New Economic Thinking at the University of Oxford (https://www.inet.ox.ac.uk/publications/empirically-grounded-technology-forecasts-and-the-energy-transition) finds that solar and wind costs continue to follow steep “learning curves”: as deployment doubles, costs fall by roughly 20 per cent. Oxford’s latest forecasts (see above) suggest that solar photovoltaic (PV) capital costs could drop by a further 30 percent in the next two decades, and wind by 15 percent in real terms over ten years. Operating costs are declining in tandem, as scale and efficiency take hold.

This dynamic — technological learning — is the single most powerful deflationary force in the energy system. Unlike fossil fuels, where prices are tied to volatile commodity markets, renewables become cheaper the more we build them. Yet our financing and regulatory structures remain largely static, locking consumers into outdated strike prices and limiting firms’ ability to pass on cost savings.

Financial innovation for the next phase – how does the CloCo Generate Alpha For Investors

To keep up, the energy transition needs a new generation of financial instruments that align incentives for investors, energy companies, and consumers. One such innovation is the Climate-Linked Convertible (CloCo) bond , developed by Dr Chris Cormack and Professor Andrea Macrina at University College London. The concept builds on the logic of convertible bonds — securities that can be exchanged for equity — but adds a climate twist.

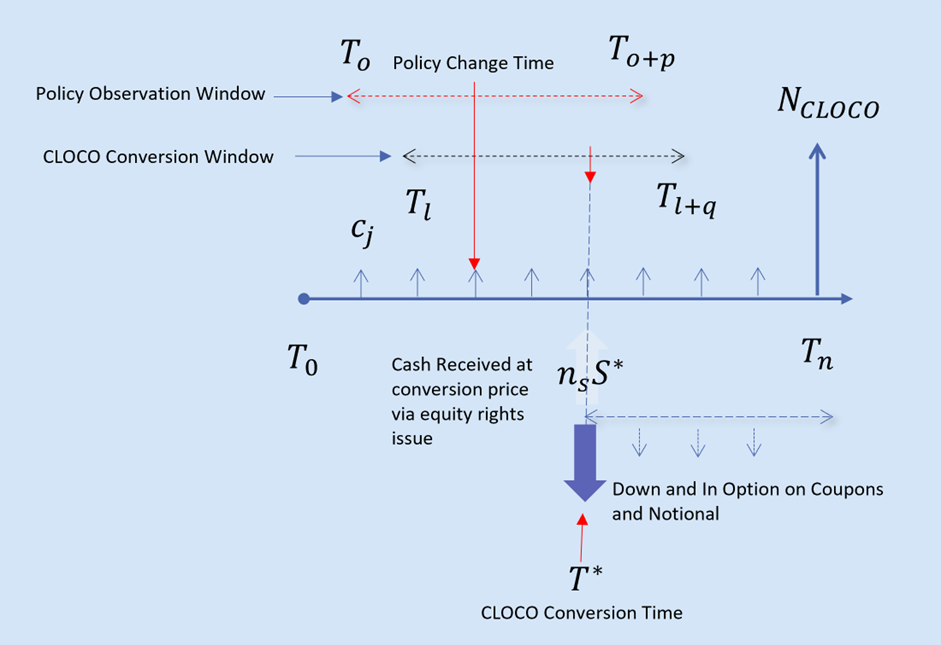

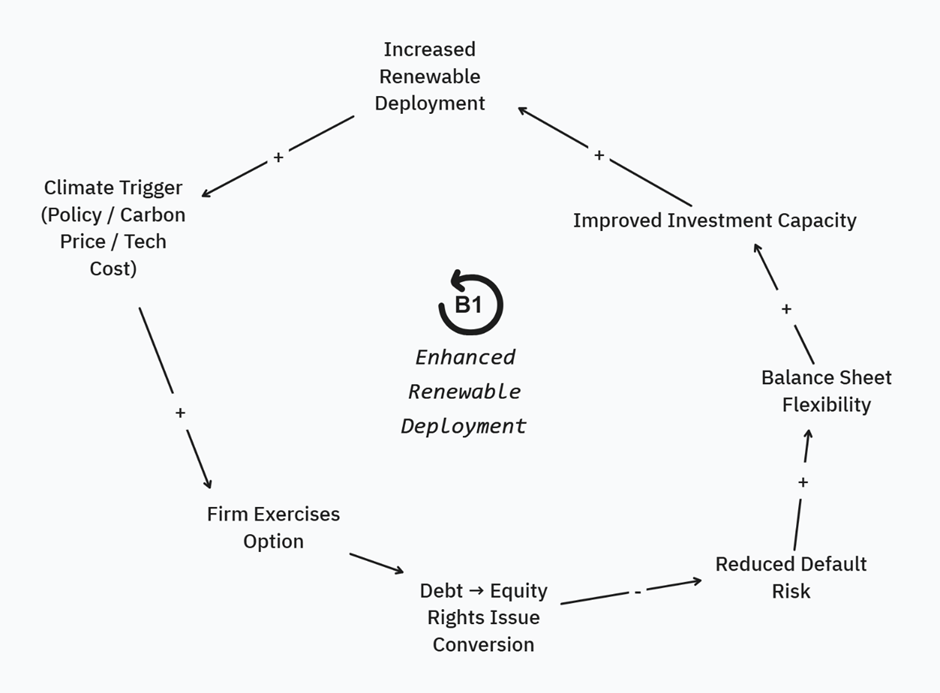

A firm issues a CloCo bond to finance low-carbon investments such as wind or solar projects. The bond behaves like a normal coupon-bearing debt instrument, but with an embedded option. If the capital cost (CAPEX) of the underlying technology falls below a pre-set trigger threshold (eg. reduces by 30% over a defined time horizon), the firm has the option to convert — via an equity rights issue supporting a nil-paid rights clause to provide bond holders a payout of the outstanding net present value of the note notional and coupons. As a consequence, the fixed income bond holder receives a cash payout, the firm cancels the associated debt (but the cash producing renewable asset remains) and The embedded optionality provides what is termed in the financial industry as structured alpha. That is the option embedded in the bond provides the bond investors an enhanced return per unit risk (eg. default risk) over a conventional coupon bearing bond issued by the firm or its competitors.

Figure 1: Cashflow diagram of the coupon bearing CloCo bond, the conversion mechanism is via a cash pay out to bond holders from the rights issue mechanism.

Generation of a Climate Alpha – Methodology

The formulae above highlights the impact on the yield of the CloCo if there is a tradable security then this would imply that the yield would be lower than a conventional bond (ie. one without an embedded option). However, as it stands there is no clearly defined tradable security that can represent the technology cost (CAPEX / OPEX). The implications from a pricing perspective is that the pricing is incomplete for investors. Hence firms in the case where there is no traded security for the technology CAPEX can chose to compensate investors for the full value of the optionality and hence provide them the full yield that matches the conventional coupon bearing bond. This is the novel source of Climate Alpha that has been designed to add value for fixed income investors and enable enhanced growth for firms and the wider macroeconomy.

This conversion effectively reduces the firm’s debt burden, freeing capital to reinvest in further decarbonization technologies at a lower per unit capital cost. Equity holders are not diluted unfairly, and the firm gains flexibility to respond dynamically to real cost improvements and deploy further assets or engage in competitive price reduction to win further contracts attracting new equity investors and stronger stewardship discussions from institutional investors.

Figure 2: The Renewables Deployment Opportunity Loop For the Firm

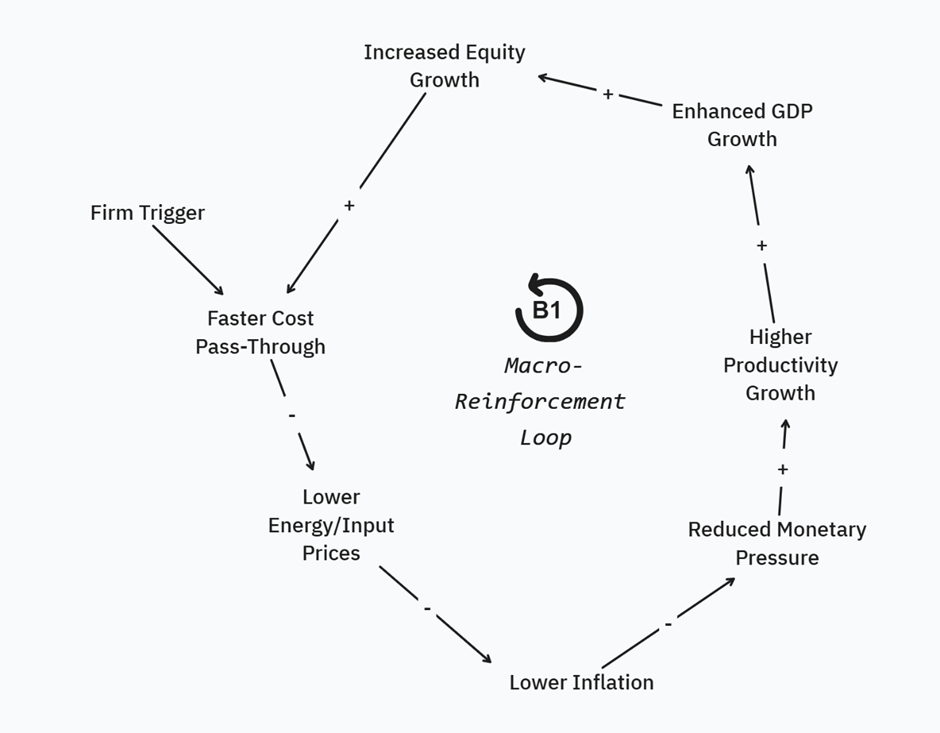

The implications ripple outward. By lowering companies’ cost of capital and accelerating the adoption of cheaper technologies, CloCos can help push down wholesale energy prices. For consumers, this can translate into tangible relief. for example, as has been observed in 2024 as energy prices reduced (eg. ONS https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/april2024) knocked a full percentage point off the U.K.’s Consumer Price Index. Cheaper energy feeds directly into lower inflation — a benefit not just for households but for the Bank of England’s monetary policy calculus.

Why electricity market policy re-design now matters as much as turbines

Financial engineering may sound remote from climate policy, but it is precisely here that the next leap must occur. The CFD model worked because it derisked early investment; the next phase should reward cost reduction and innovation. If policymakers allow CFD contracts to “re-strike” downward when firms deploy capital-efficient technologies — particularly those financed through transparent structures like CloCos — they can embed a virtuous cycle: cheaper capital leads to cheaper power, which leads to lower inflation and faster decarbonization.

Such reforms would not require vast new subsidies. They would, instead, reward firms for delivering technological progress and passing savings to consumers. In a fiscally constrained environment, that kind of policy precision is gold dust. McKinsey estimates (https://www.mckinsey.com/capabilities/sustainability/our-insights/the-net-zero-transition-what-it-would-cost-what-it-could-bring) that global investment required for the net-zero transition will exceed USD 9 trillion annually by 2050, far above current flows. Yet every percentage point reduction in the cost of capital unlocks billions more in feasible projects.

Figure 3: Macro-Economic Opportunity Loop with Electricity Market Reform for Consumers and Industry

The geopolitical dividend

The benefits of smarter financing extend beyond the U.K. The United States’ Inflation Reduction Act turbocharged investment by coupling fiscal incentives with industrial strategy. Even now renewables are gaining ground in states such as Texas and beyond due to the lower cost of production and investment opportunities, the CloCo has been designed to address in part the challenge of climate policy but to facilitate further opportunities for any economy. Within Europe for example, the challenge is to match that pace without ballooning public debt. Instruments like CloCos — and broader public-private blends that shift risk without heavy fiscal cost — could give European markets a much need economic boost.

The geopolitical stakes are high. Economies that can deliver low-cost, low-carbon electricity will dominate the next industrial cycle, from AI to heavy industry and beyond. Those that fail to optimize their financial architecture risk watching capital, and competitiveness, flow elsewhere. For Britain, the prize is doubly valuable: lower energy prices could not only underpin productivity growth but also ease inflationary pressure, giving the Bank of England more room to manoeuvre and the Treasury a path to fiscal credibility.

The wider view: a financial architecture for climate stability

At heart, the energy transition is a race between technological possibility and financial friction. Renewables can now outcompete fossil fuels on cost, but the legacy of old contracts, slow regulatory feedback, and rigid capital structures threatens to slow deployment and inflate prices. Financial engineering — often maligned since the global financial crisis — can, when used judiciously, become the missing lever of macroeconomic stability.

Embedding adaptive pricing mechanisms, climate-linked bonds, and smarter public-private risk sharing into the energy system can deliver deflationary tailwinds just when economies need them most. The outcome would be lower energy costs, enhanced investment confidence, and accelerated progress toward net zero — all without exacerbating fiscal deficits.

The U.K. has long been a global laboratory for market-based climate solutions, from its pioneering carbon trading schemes to its leadership in offshore wind. By marrying that ingenuity with new tools like the CloCo and adaptive CFDs, it could again lead the world — this time not just in cutting emissions, but in designing a financial system that makes decarbonization an engine of growth rather than a cost to be borne.

As policymakers look ahead to the next phase of the energy transition, they would do well to remember that markets can be tamed — and turned — by design. The physics of climate change may be immutable, but the economics of energy are ours to shape.

Dr Chris Cormack is a climate finance entrepreneur and quantitative modeller specialising in systemic risk and macro-financial climate analytics. As founder of Quant Foundry Limited, he develops firm level agent-based models for banks, asset managers and insurers enabling the, assessment of physical and transition linked climate risks. He is Co-Creator and commercial owner of the Climate Contingent Convertible (CloCo) bond to accelerate renewable deployment while enhancing investor returns. His work supports regulators, banks, and policymakers in aligning financial stability with climate transition.